From numerous sides arguments can be heard, about how since the time of communism nothing changed in the Slovak economy, and that the effort of reforms that run through the past twenty years and mainly since 1998, didn't bring any positive results. In this lecture I would like to attend to the process of reforms and their result. This analysis is even more important, because Slovakia as well as the western Europe in the past years went through a painful economical crisis that reversed some positive trends.

The lecture has two parts:

- short economical history of the reforms in Slovakia

- economical consequences of our reforms

A short history of the reforms in Slovakia

Firstly, it’s not possible to identify the whole season after 1989 with reforms. The phase of transitions didn’t go evenly from the perspective of changes.

In the first free parliamentary elections in June 1990 the pro-west orientated parties with a program including the liberalisation of economy clearly won. In January 1991 the federal government prepared the basis for a fast liberalisation of prices, salaries and market, which were successful in the settling of a macroeconomical imbalance. Considering the real business development was this policy less successful, at least when it comes to Slovakia. As well as all transforming countries, Czechoslovakia too, noted a time of deep recession and rapid decrease of production in 1991-1992. The cause of this development (and similar trends in this phase of a recession) was the break-up of the internal and external economical relationships and mechanisms, including the collapse of the key foreign markets, especially in countries of the old Comecon. However the consequences of this development were imbalanced. The Slovak economy was hit harder than the Czech one, since it became more dependant on the markets of the Comecon due to the industrialisation during communism, and so was in the position of the executor of mineral resources and producer of the simpler raw products. That’s why was the recession in the transition time in 1991-1992 in Slovakia more dramatic, with a decline of production by more than 20 percent and unemployment exceeding the 10 percent line, which was in both cases twice as high as in the Czech republic.

In the time between 1992-1998 were the reforms and the economical restructuring to a great amount stopped. The government of Vladimír Mečiar focused on the short term solutions and on the privatisation in favour of their political allies. The result was, also considering the revival or the west-european economy, a short phase of fast growth, followed by the fall of the economy.

After the elections in 1998 – at the beginning of the first Dzurinda’s government – the state of the Slovak economy was characterised by a great deficit of the national funds and balance of payments, depreciation of the currency and until 2002 they managed to renew the macroeconomical stability and slightly strengthen the economical growth. The banks and network branches were restructured and the majority of them privatised. In 2000 became Slovakia a member of the OECD (five to six years after their middle-european neighbours) and at the same time acceded to the discussions about becoming a member of the EU. The time between 1998-2002 can therefore be seen as the time of catching up of the lag and the following consolidation of the economy. Despite that some system problems stayed unsolved, mainly the ones concerning the effectiveness of the use of the public resources.

The period between the end of the year 1998 and beginning of 2000 was a hard landing. In year 2001 followed a slight recovery. Efficiency measures introduced by the government in an effort to decrease the deficit of the public funds contributed to a slower economy. The government agreed to a program of stabilisation and system changes. The decrease of the funds deficit and the decrease of the household consumption contributed to a temporary and strong reduction of the external imbalance in the period between 1999 and 2000. A part of the systematic changes was the increase of regulated prices and indirect taxes in the period from 1999 to 2000, which together with the devaluation of the crown temporarily started the growth of the overall inflation.

The period of years 1998-2002 was also a period of a point-blank business reconstruction. Big national banks, up to year 1998 practically insolvent, were, together with many network branches, consolidated and privatised. The income tax of the corporate entities was gradually lowered from 40 to 25 percent. The government also introduced improvements in the juridical area in an effort to improve the business management. This, on one hand implied a much lower value of capital for the profiting and growing businesses, on the other hand however it brought a loss of financing based on political decisions. The government made crucial steps in an effort to attract foreign capital through the privatisation of banks and network branches, as well as through the help of project on green meadows. Many domestic owners of industrial businesses sold them to strategic foreign investors.

The period of years 2002-2006 is described as the end of the transformation. Even though the parliamentary elections in 2002 brought a continuity in the economical policy, the periods of two Dzurinda’s governments are usually viewed independently. The details can be mainly seen in the deepening of the privatisation and deregulation reforms, as well as in the lasting improvements of the economical situation and business environment.

However on the other hand there are two differences. The first is a considerable faster growth. System changes from the first Dzurinda’s government started to bring results. The real growth of the GDP was on average 6 percent in the period from 2002 to 2006, with an increase to 9 percent in 2006. the growth was supported mainly by a high inflow of direct foreign investment (DFI), mainly in the car industry, electronic and machine industry. Inflow of DFI and the by it caused rapid increase of the production capacity, in combination with the inflow of finances from the EU resources after 2004, stimulated the construction and boom in the domestic consumption. A more distinct growth and an ambition to become a member of the Euro-zone before 2009 additionally boosted the planned fiscal consolidation.

However the key difference between two governments is the emphasis on the reforms directed at the sustainability of the public funds. The tempo of the fiscal consolidation in the time between 2002-2003 was rapid. The deficit of the public funds decreased from 8.2 percent GDP in 2002 to 7.2 percent GDP in 2003. The budget reform package for year 2004 was directed towards the increase of the effectiveness and efficiency of the use of the public funds as well as the guarantee of the long term sustainability of the public funds. It was reforms in the following areas: tax policy, social policy, public health and education.

The parliamentary elections in 2006 were won by the opposition parties led by SMER, by which the government composition completely changed. However compared to year 1998 it didn’t come to any radical change in the economical policy – the changes were much smaller, than the majority of spectators expected. The business growth was further dynamic, the employment gradually increased, accompanied by a macroeconomical stability and low inflation. At the same time the fiscal policy kept a mild pro-cyclical tendency, while the deficit of the public funds stayed the same, more or less 2 percent GDP yearly in the period between 2003 and 2008 (besides year 2006).

Changes in the economical policy compared to the second Dzurinda’s government were noticeable mainly in the areas of public health, where the government limited the private health insurance companies. In the area of social policy the government also partially reversed some of the main steps of their predecessor, mainly the ones dealing with labour market (Labour Code, collective bargaining) and pensions, when they opened the entrance and exit into the second pillar. However the greatest turn happened in the area of privatisations, where the new government (at that time) cancelled all unfinished transactions and blocked all other possible privatisations. Instead of that has the new government tackled projects of the public-private partnership (PPP) and public investment.

At the end of year 2008 has the global financial and business crisis in Slovakia fully manifested. The government reacted to it by an expansion of the fiscal policy, which led to the growth of the deficit in the public funds to 8% GDP in years 2009 and 2010. The increase of the primary deficit of the public funds actually belonged to the highest ones in the EU. Even despite of that it failed to prevent one of the fastest growths of unemployment in the union. There were discussions in the professional community about to what amount is this development the result of an export sensitive structure of the economy and to what amount it is the result of a badly set business policy. In year 2010 started the economical renewal and a yearlong growth of the GDP in year 2010 should reach up to about 4%. However the government of Robert Fico was in June 2010 replaced by the government of Iveta Radičová after the lost parliamentary elections in June 2010. The loss was a consequence of the effect of the crisis and greatly increased corruption that became one of the key topics at the elections. However the new government coalition effective from 2010 wasn’t capable to stay in power for longer and fell after about a year and half. In that time it managed to make mainly the ambitious fiscal consolidation and Labour Code reform. Other planned essential reforms – levy, universities, public health – were stopped by the early elections. On the other hand, the government of Iveta Radičová implemented a high number of extremely ambitious anti-corruption reforms.

Economical consequences of the reforms in Slovakia

Business growth, country and (im)balance

In this part we look at the business growth and size of the country. The data confirms, that from year 2004 Slovakia is consistently overrunning its neighbours in the growth. This growth was preceded by a radical reduction in the size of the country.

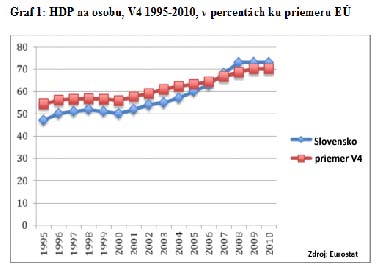

Towards the end of the twentieth and beginning of the twenty-first century was the growth of the real GDP per person in Slovakia nearly comparable to the one of the neighbouring countries (neighbours), however the individual amount of income was lower (graph 1). The real GDP per person radically increased since 2004, increasing the income per person compared to the EU; since 2007 was in Slovakia the income per person higher than the average of V4. In year 2009, the real GDP per person in Slovakia reached by 3.2 percent more than the average of the countries of the V4 in the same period, however Slovakia in 2009 lagged behind by 30 percent after the average of the EU 27 GDP per person (Eurostat).

The key factors affecting a more distinctive growth of Slovakia in the past years are mainly the result of radical systematic changes introduced by the previous governments, rapid fiscal consolidation and with it linked reduction of the size and influence, as well as the critical improvement of the effectiveness of the use of the public funds.

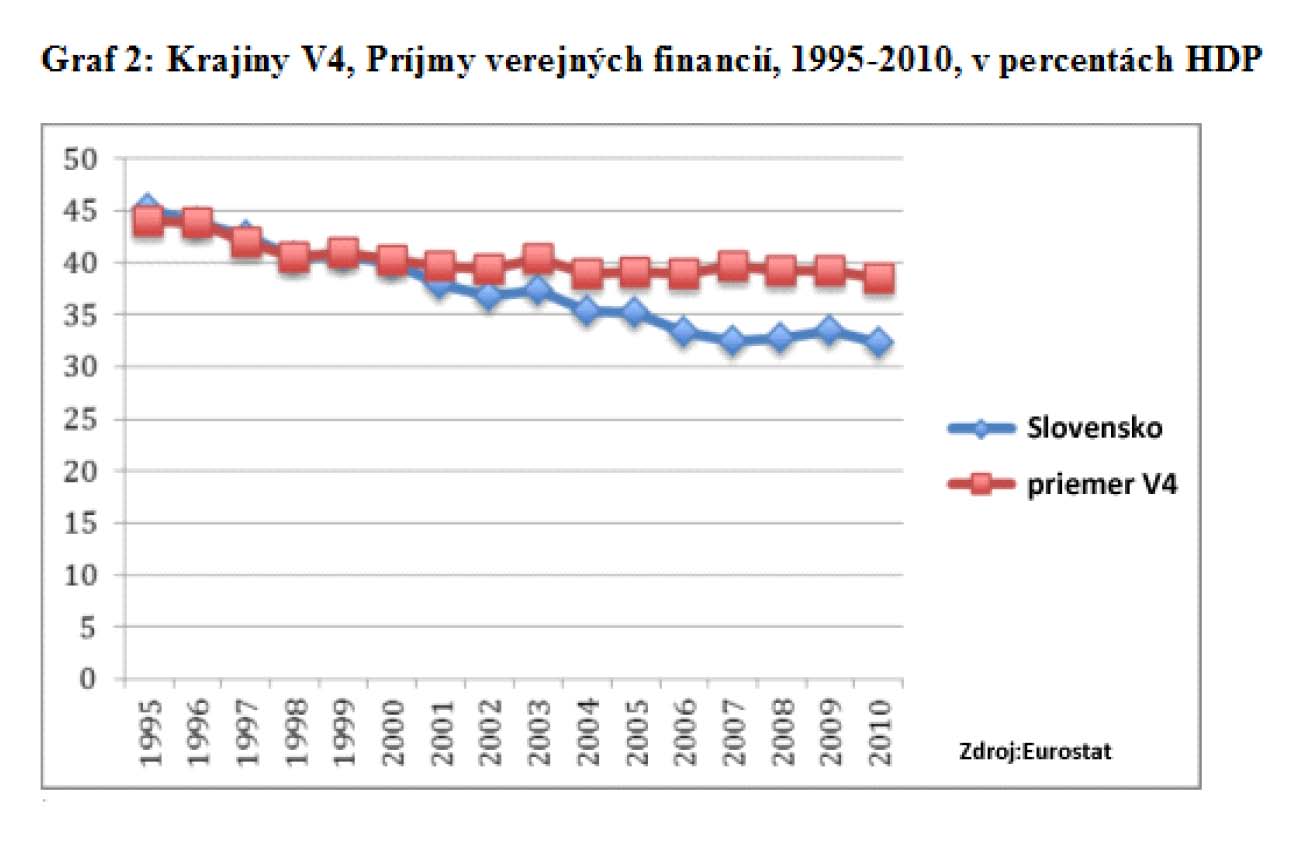

Graph 2 compares the incomes of the public funds in Slovakia compared to the average of V4. Until 2000 the public incomes relative to the GDP were more or less the same. However in the last decade, 2000-2010, has the average of the V4 kept stable at about 40 percent GDP, while the income of Slovakia decreased to a level under 35 percent GDP.

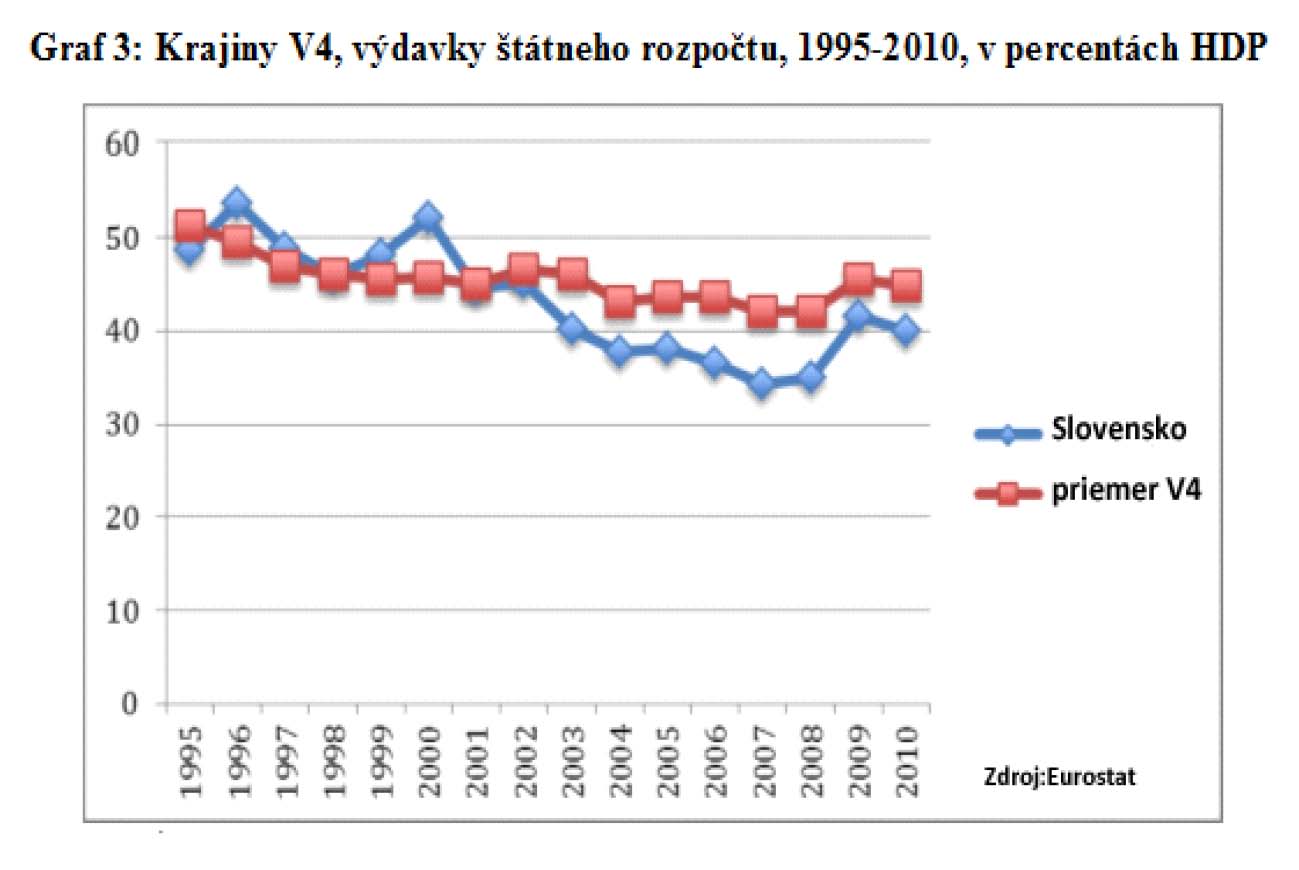

The development of the expenses was even more dramatic: in years 1995-2010 Slovakia noted the greatest decrease of the public expenses in the EU. In year 2009 the Slovak government spent around 4.5 percent GDP less that the average of the V4 in 2009 (Graph 3). At the same time up until the crisis Slovakia managed to lower the fiscal deficit and the long term sustainability of the public resources improved. (European commission evaluated Slovakia in the context area of the sustainability of the public funds as a country with moderate risk (EK, 2006, p.86). The crisis dramatically worsened the situation of the public funds, but didn’t change the grounds of the Slovak fiscal model.

Business environment and direct foreign investment

Slovakia noted two very distinct shifts in the field of privatisations and business policy. The first happened in the middle of the nineties, when the coupon privatisation and liberal business policy were replaces by the privatisation in favour of the business groups and business policy, that kept the selected companies over the edge with the help of national banks, which also co-financed the privatisation. To the second shift came at the end of the nineties, when this model got replaced by the bank privatisation, (re)privatisation of the production companies and network branches by the foreign investors, as well as the explicit support of the direct foreign investment at the “green meadow”. These measurements were later replaced by the by market accepted measurements directed at investment and development of the business environment (including, but not exclusively measurements dealing with a lower tax burden and improvement of the regulation environment). The government, that came to power after the elections in 2006 may have stopped the privatisation, but the remaining share of the non-privatised properties stayed relatively small.

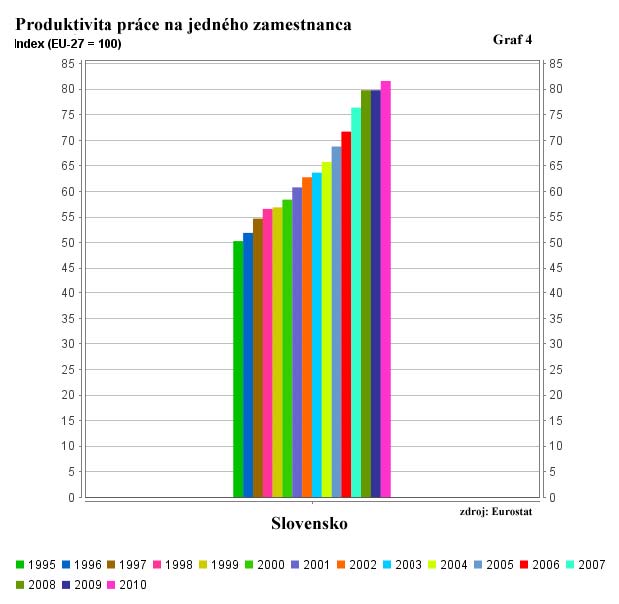

If we take a closer look at the question of productivity we will notice that during years 1995 and 2010 Slovakia gradually came closer to the average of the European union. (graph 4). Increase of the work productivity in Slovakia is closely linked with the increase of the direct foreign investments.

Slovakia managed to keep a high share in the commercial banks (around 50 percent from the overall amount) even during the second half of the nineties while the regional one decreased (graph 6). When the reconstruction and privatisation of the national banks started, during one year the national ownership decreased to nearly zero. This trend is again an example of the change in policy after the elections in 1998.

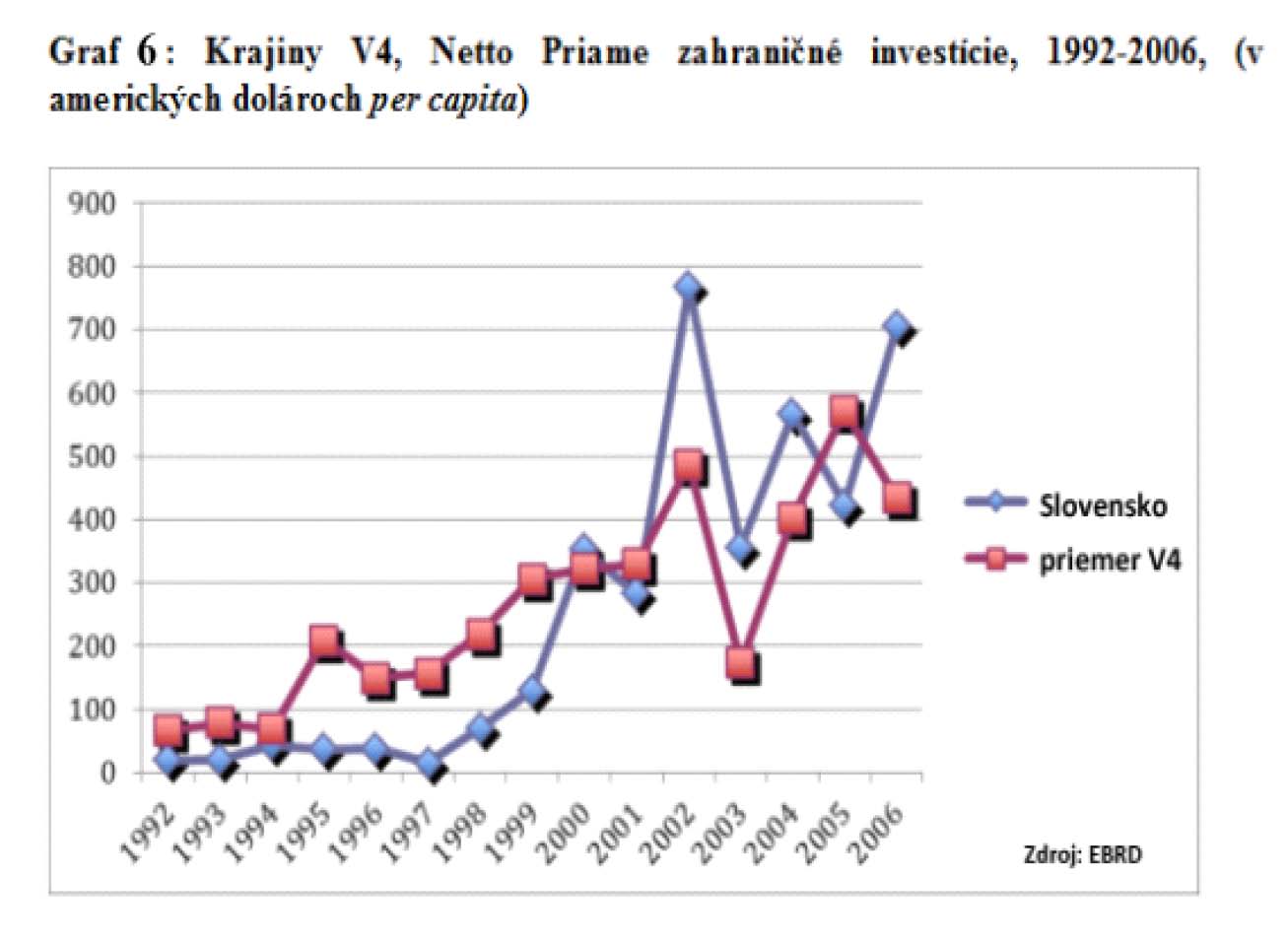

In the period between 1994-1999 Slovakia attracted the least direct foreign investments out of the countries of the V4 (Graph 7). However since 2000 Slovakia managed to even out these differences and since then attracts more direct foreign investment than the average of the V4).

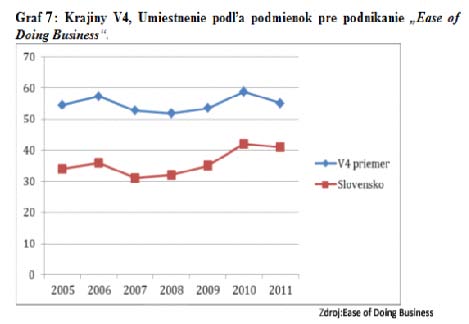

In the overall measure the data confirms, that during the first Dzurinda’s government Slovakia noted essential shift in the economical policy, when the country in parallel reconstructed and privatised banks and network branches, started to attract direct foreign investment and started to catch up to its neighbours in productivity. Even though the structural reforms of the second Dzurinda’s government and the emphasis on the macroeconomic stability during Fico’s government (up until the crisis) were important, in the business sphere they based on the robust ground set in the time between years 1999 and 2002. As a result of this, Slovakia has currently the most liberal business environment out of all middle-europe countries (Graph 8). According to a study of the World bank Doing Business 2011 will Slovakia do better by one rank and will move to the 41st place, at the same time it will stay before other countries of the V4. However, worth mentioning is the fact, that the other countries of V4 have been catching up to us since 2008. For example the Czech improved by 19 ranks in the last year. Similarly, while in 2007 was the difference between Slovakia and Hungary 20 ranks, according to the prognosis for year 2011 will Hungary come closer to a difference of only 5 ranks. Slovakia achieved the highest ranking in the evaluation of the Doing Business in years 2004 and 2005, where it ranked within the first ranks between the best world reformers of the business environment.

Conclusion

If someone claims that nothing has changed in Slovakia in the past few years and that reforms didn’t bring anything – they simply aren’t telling the truth – or they are closing their eyes before the facts. Sometimes people forget the hard work, that’s why, lets conclude the knowledge from today’s lecture.

After the slow start of Slovakia, often even in a reverse, came a very hard landing in years 1998 till 2000. Followed by a rapid business reconstruction, which brought to Slovakia a rapid growth, inflow of direct foreign investments, decrease of the deficit of the public funds and in Europe and in the world the reputation of an admired reformer. Since 2004 Slovakia has been defeating its neighbours in growth and even despite of a high amount of poverty is the level of imbalance lower than in Poland and Hungary.

The data confirmed, that during the first Dzurinda’s government Slovakia noted an essential shift, when the country in parallel reconstructed and privatised banks and network branches, the country started to attract direct foreign investments and those again helped to increase the productivity of the Slovak workers. It’s also the result of these laid-down stable bases why Slovakia currently has the most liberal business environment out of all the middle-European countries.

The success of the reform governments can be also measured indirectly and the deepest blow has been paradoxically given by the new government in 2006. Despite of the declared interest, it didn’t come to a radical change of the overall economical policy. But it came to changes in the social, public health policy and the stopping of privatisation. The government of Robert Fico targeted in this business policy vision mainly projects of the public-private partnership, also known as PPP. Slovakia went in years 1995-2009 through the greatest decrease of the public expenses, and this on a whole-European level.

We started to intensively feel the consequences of the work business crisis in 2008. It came to the increase of the public funds deficit and a rapid increase of unemployment. This fall probably cost Robert Fico another election and the more distinct part- the so called reform working forces, came back to power. However the government managed to keep their power for one and half years and the early election are there again due to the world business crisis and its geopolitical consequences.

Comments

4 comment(s). Display all comments.

to ze sa motame dokola je pravda, co pravica opravi to lavica pokazi, ludom to dojde a zavola pravicu, ta robi nepopularne opatrenia co po case nasrie ludi a zvolia si populistov z lavice a tak dokola… :(

Tvoj pohlad je velmi kratkozraky, myslis si, ze som taky hlupy, ze chcem brat pracu ludom? Vdaka ludom, ako si ty, mladi ludia musia dnes striekat v Bratislave Volkswageny namiesto toho, aby sa prechadzali po lesoch a davali pozor na nase najvacsie bohatsvo, vdaka tvojim nazorom zo Slovenska ludia vo velkom odchadzaju a rodiny sa z nedostaku penazi rozvadzaju, pretoze pracovne pomery v zahranicnych pasovych halach su odporne, namiesto toho, aby ludia sedeli v garazi a zivili sa drobnymi remeselnickymi pracami, tak ako tomu bolo v dobe, ked sa na Slovensku zilo dobre a ked sa zakladali rodiny a ludia boli k sebe slusni a mili. Ale to by si sa musel najskor v skole dobre potrapit, aby si na toto vsetko prisiel.

Keby tu neboli zahraničné podniky, tak kto by dal ľuďom prácu? Myslíš, že v slovenských podnikoch ľudia nemakajú? S Maďarmi by som Slovákov neporovnával, pretože majú úplne iné podmienky ekonomiky. Sú viac sebestačný a ich ekonomika je väčšia než naša. V posledných rokoch sú navyše na pokraji bankrotu, čo sa odrazí v horšej budúcnosti a to uvidíš, ako potom budú musieť makať, aby sa mali lepšie. Radšej je lepšie si brať príklad z podobných ekonomík, ktoré majú svetlú budúcnosť ako hlavne Estónsko.

Tazko sa niekomu, kto ma plat niekolko tisic eur vysvetluje, ze beznemu obcanovi ide v prvom rade o to, aby mal pracu, ktora ho bavi aj za cenu nizsieho hdp ako to, ze sice makroekonomicke grafy mame najlepsie, ale ludia sa musia neporovnatelne viac namakat v halach zahranicnych investorov. Ludia dnes nemozu podnikat, pretoze to stat svojimi reformami znemoznil, ale ludia musia posluchat zahranicnych nadriadenych… Polopate povedane Madar sa ma rovnako ako my, ale s tym rozdielom, ze cely den sa vala na poli a pestuje si papriky, ale Slovak maka ako kon… Ale toto nepochopia ludia ako Miklos, Beblavy atd.

Avsak niektori ludia tomu velmi dobre rozumeju, napriklad byvali poradcovia prezidenta Schustera kritizovali jednotnu dan, byvaly riaditel socialnej poistovne ktitizoval druhy pilier a aj dalsi z aliancie podnikatelov, ale nikto ich nepocuva…..